The strike on South Pars—the world’s largest natural gas reserve, shared between Iran and Qatar—crossed a threshold that energy markets had treated as a tail risk and priced accordingly. Iran’s retaliation was swift and geographically broad: missiles and drones targeted energy facilities in Qatar, Saudi Arabia, and across the wider Gulf. By Thursday morning, Israeli Prime Minister Netanyahu claimed Iran can no longer enrich uranium or manufacture ballistic missiles. Markets registered the claim, then kept moving.

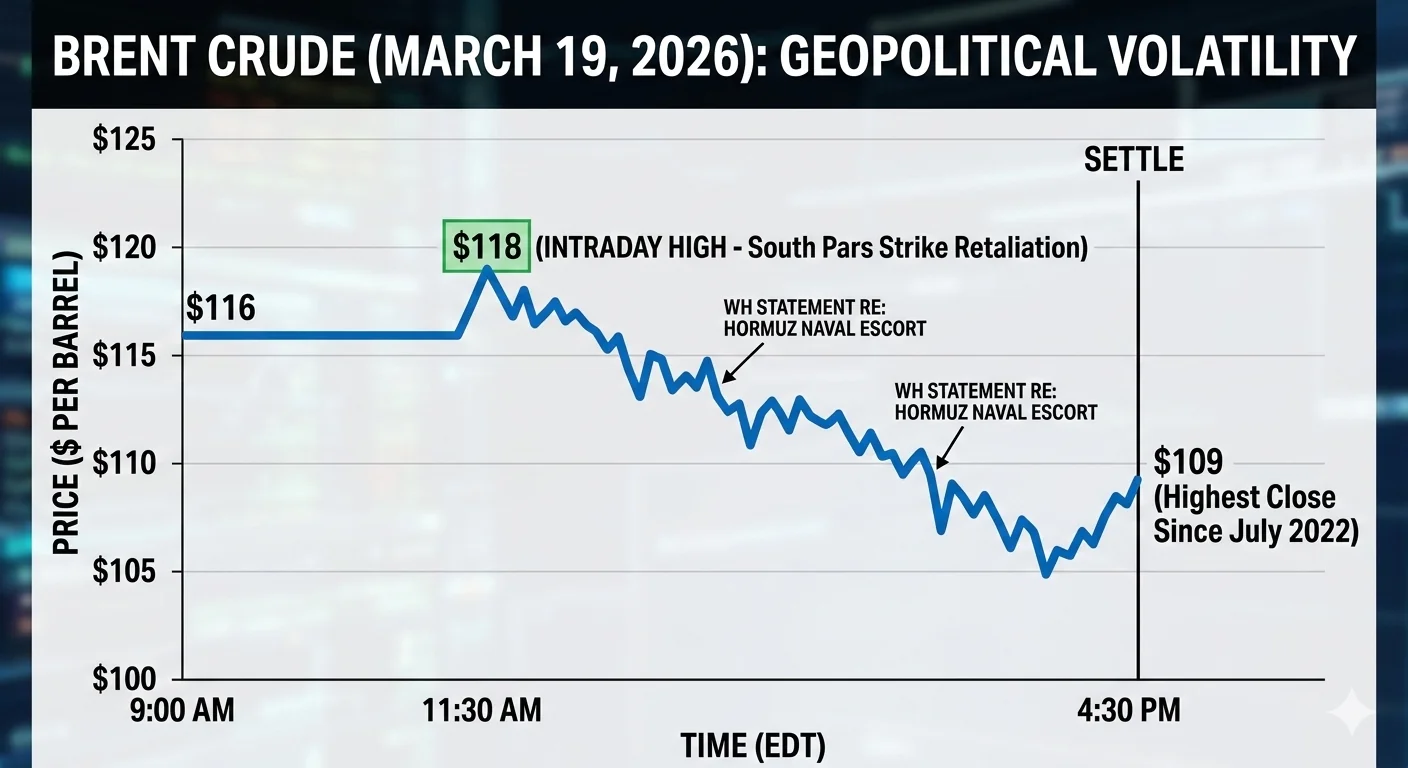

Brent crude reached $118 per barrel in early Thursday trading, its highest intraday level since July 2022. It pulled back to settle at $109 by session close—tracking White House statements that restoring flow through the Strait of Hormuz was a top priority, and that Israel would assist with naval escort operations. The S&P 500 slid 0.27% on the day. It was the second consecutive losing session for all three major averages.

The Strait Is the Mechanism, Not the Headline

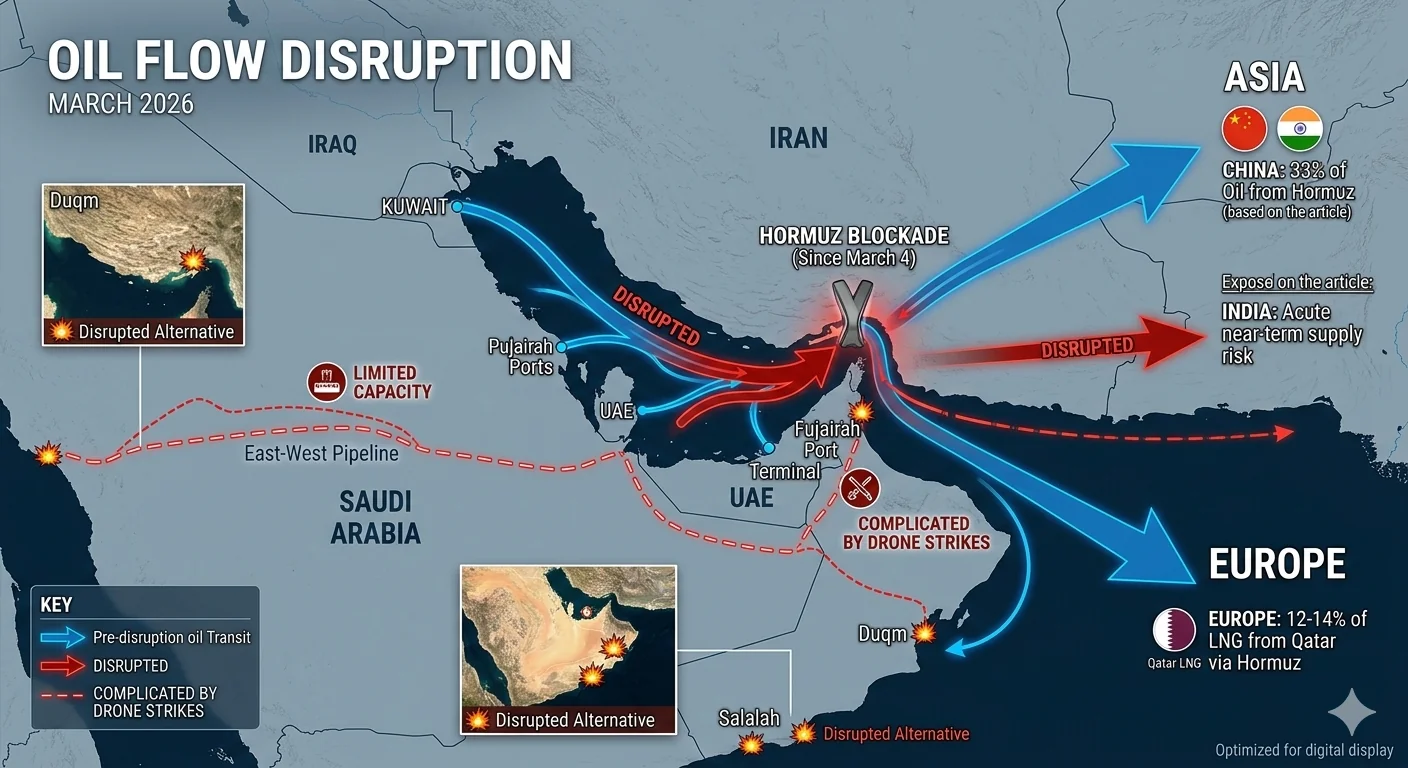

South Pars matters. But the Hormuz closure is the actual constraint on global energy supply—and it predates Wednesday’s strike by two weeks. Since March 4, Iranian forces have enforced a de facto blockade against vessels linked to the United States, Israel, and their allies. Daily transits through the strait have fallen from a historical average of 138 ships to fewer than five. At its narrowest point, the waterway is 21 miles wide—a corridor through which roughly 20% of global seaborne oil and one-fifth of global LNG supply normally passes.

No alternate route replaces that volume. Saudi Arabia’s East-West Pipeline and the UAE’s Fujairah terminal offer partial detours, but their combined throughput capacity falls far short of a full Hormuz substitute. Iranian drone strikes have already hit two of the primary bypass ports—Duqm and Salalah—complicating even those alternatives. The shipping industry’s verdict has been blunt: commercial operators, major oil companies, and insurers have withdrawn from the corridor entirely. Insurance premiums reached a six-year high before the war began. Now many underwriters won’t price the route at any premium.

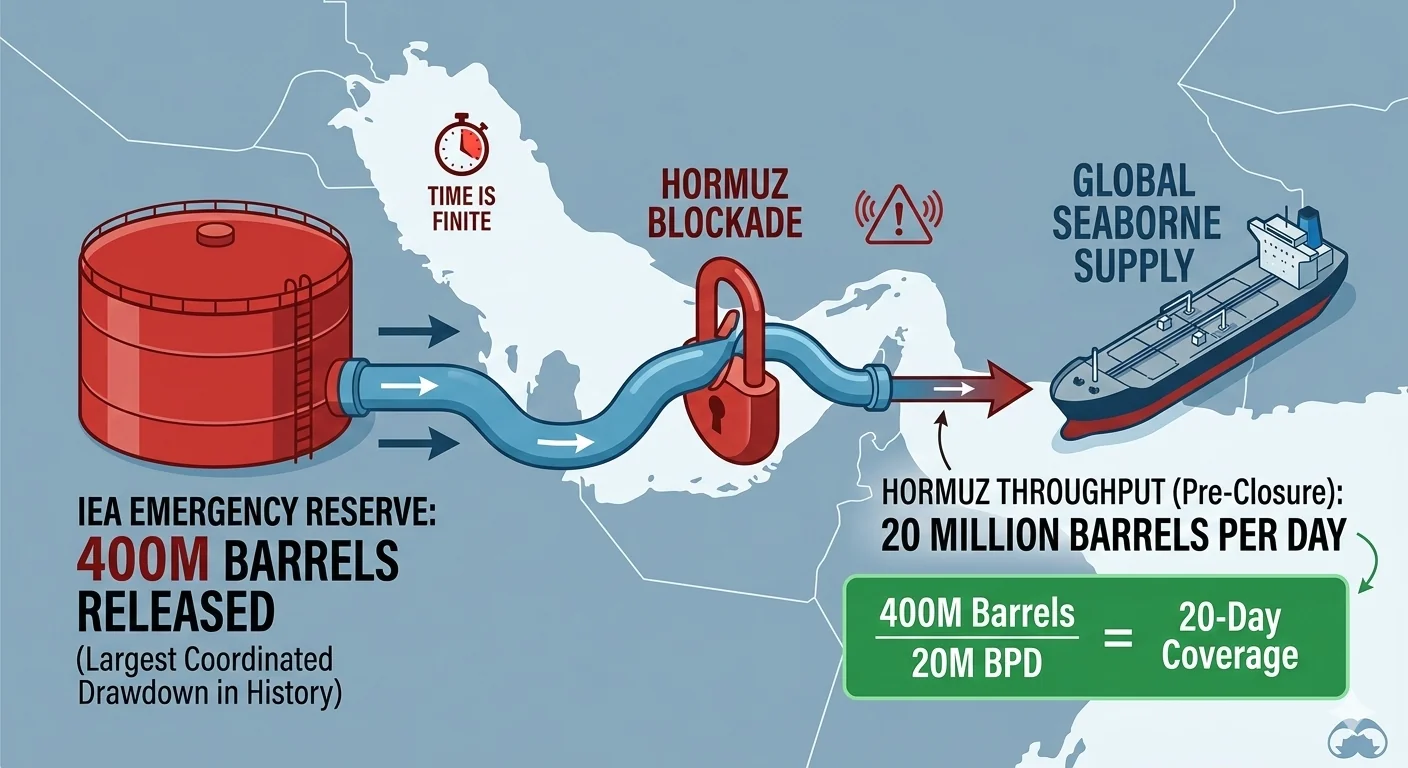

The International Energy Agency responded by releasing 400 million barrels of emergency reserves—the largest coordinated drawdown in its history. The math is sobering. Normal Hormuz traffic runs around 20 million barrels per day. Those reserves buy roughly twenty days of replacement coverage. They cushion the shock; they do not fix the underlying disruption.

A Coalition Without Volunteers

Trump has called on China, Japan, France, and the United Kingdom to deploy naval escorts through the strait. None has publicly committed. Japan and Australia said Monday they had no plans to send ships. The American Petroleum Institute’s president, speaking Thursday on CNBC, called reopening Hormuz a matter of national urgency. “There is just no substitute right now,” he said.

The geopolitical structure of the impasse is worth pausing on. The countries most exposed to prolonged Hormuz closure—China receives roughly a third of its oil through the strait; India faces the most acute near-term supply risk—have the weakest incentive to join a US-Israeli naval mission. Europe, which sources 12 to 14 percent of its LNG from Qatar through the strait, is watching. Russia benefits from every additional week of disruption: both India and China are already pivoting back toward Russian crude as Middle Eastern barrels become inaccessible. The crisis is restructuring Asian supply chains in ways that may persist well beyond any eventual ceasefire.

What the South Pars Strike Changes

South Pars holds an estimated 1,800 trillion cubic feet of natural gas. Wednesday’s strike was the first time Israel targeted Iran’s primary gas export infrastructure directly. Trump told reporters the United States “knew nothing” about the operation. Axios reported, citing Israeli and American officials, that the strike was coordinated with and approved by the White House. Both statements cannot simultaneously be true.

With Netanyahu claiming Iran’s enrichment capacity and ballistic missile production are degraded, Tehran’s strategic position narrows. A sealed Strait of Hormuz becomes one of its few remaining pressure levers—which gives Iran little incentive to reopen it until its own calculus changes. The IEA drawdown, the US military posture, and the diplomatic silence from potential coalition partners all point toward a prolonged standoff rather than a rapid normalization. Macquarie forecasts no Fed rate cuts in 2026 and marks the next likely move as a hike—oil above $100 into spring only hardens that call.

The Strait of Hormuz has functioned as the theoretical chokepoint of the global oil market for fifty years. The working assumption was always that no actor would fully close it, because the economic damage would be mutual. That assumption has now been tested. The closure began seventeen days ago, and the strait is still closed.

Tags

Related Articles

Sources

Reuters, Bloomberg, Al Jazeera, CNN, Congressional Research Service, Kpler, IEA, CNBC, Wikipedia (2026 Strait of Hormuz crisis)