The AI industry has solved distribution. It has not yet solved economics at the consumer edge.

ChatGPT processes billions of requests weekly. OpenAI reports roughly 900 million weekly active users and on the order of 50 million paying consumer subscribers — a free-to-paid conversion rate near 5.5 to 6 percent. Revenue is real: subscription annual recurring revenue crossed $10 billion in 2025, with enterprise and API lines now representing more than half of total receipts and climbing toward parity with consumer by year-end 2026. The product works. People use it. The question is whether usage intensity and wallet share scale with the megawatts being committed upstream.

That gap — between reach and revenue, between demo delight and durable payment — is where ghost warehouses live.

What “Utility” Means in This Cycle

Utility is not the same as capability. A model that drafts acceptable emails has utility. A model that justifies a $725 billion hyperscaler capex guide has to do more: replace labor hours billable at enterprise rates, compress software cycles, or unlock new products consumers renew for monthly.

Three layers of utility matter:

Task substitution. Does the tool reliably remove minutes from a paid workflow — coding, customer support, legal review, radiology triage — at a cost below the labor it displaces? Enterprise retention near 88 percent on ChatGPT Enterprise contracts suggests yes, for a defined cohort. Consumer Plus retention near 59 percent at twelve months suggests enthusiasm fades faster at $20 per month.

Habit formation. Free tiers create traffic. Paying tiers require daily return value — the assistant must be faster than search, cheaper than a freelancer, or embedded in software the user already opens. Traffic without habit is the dot-com pattern: eyeballs that never monetize.

Price elasticity. Apple raising Mac prices and Microsoft hiking Xbox hardware as memory costs surge shows AI scarcity transmitting downstream. If the consumer product cannot pass through its own cost inflation, margin compression arrives before obsolescence does.

The honest read: enterprise utility is further along than consumer utility, and the buildout is priced as if both were further along still.

The Engagement Threshold Hyperscalers Need

No public company publishes a single “break-even queries per user” figure. But the arithmetic is inferable.

Hyperscalers are projected to spend $450 billion to $775 billion on AI infrastructure in 2026. OpenAI alone targets 220 million paying users by 2030 — a sixfold increase from today’s base. At blended average revenue per user near $25 to $40 per month across Plus, Team, and Enterprise tiers, that ambition is coherent if conversion rises and churn falls. If conversion stalls at 6 percent while weekly actives approach a billion, the industry is building for a audience that treats AI as a free utility — like search in 2004 — not a subscription product.

What paying engagement likely requires:

- Conversion above 10 percent on mature consumer cohorts, or aggressive ad and API monetization of the free tier (OpenAI’s ads line is still roughly 1 percent of revenue but projected to grow).

- Net revenue retention above 120 percent in enterprise — seat expansion on renewal, not logo churn masked by new sales.

- Inference utilization above 50 percent on deployed GPU fleets. Surveys place enterprise GPU utilization between 5 and 30 percent today; racks that idle while power bills run 24/7 are balance-sheet poison.

Sam Altman has framed 2026 as an application problem, not a training problem. That is an admission: model capability outran product-market fit at consumer price points. The binding constraint shifted from “can we build it?” to “will they keep paying for it?”

If Utility Fails: Ghost Warehouses, Not Empty Fields

The telecom bust left dark fiber — capacity that existed but earned nothing. AI’s version is more expensive per square foot.

Physically dark racks. Facilities in Northern Virginia and Texas have shipped GPUs while waiting months or years for energized transformers and switchgear — an estimated 12 gigawatts of planned capacity in “power limbo” as of mid-2026. A building 90 percent complete but 0 percent powered bleeds carrying costs while silicon depreciates in sealed crates. That is a ghost warehouse in the literal sense.

Architecturally stranded sites. Microsoft canceled or deferred more than 2 gigawatts of data center agreements between late 2024 and early 2025 — not because AI demand vanished, but because committed designs misaligned with shifting workload mixes. Training-centric mega-sites do not cheaply convert to latency-sensitive inference at the edge. Purpose-built liquid-cooled GPU halls are closer to custom smelters than to general office space.

Financially impaired assets. Stranded infrastructure is not always abandoned concrete. It is often a repriced power contract, interconnection right, or debt package attached to a facility that earns commodity margins instead of monopoly rents. Sites with durable fiber and flexible cooling survive. Sites built for permanent H100 scarcity do not.

North American data center vacancy dropped below 2 percent in 2025 with most new capacity pre-leased — so the near-term risk is not mass emptiness but margin compression and write-downs on the wrong assets in the right boom.

What Happens to the Equipment

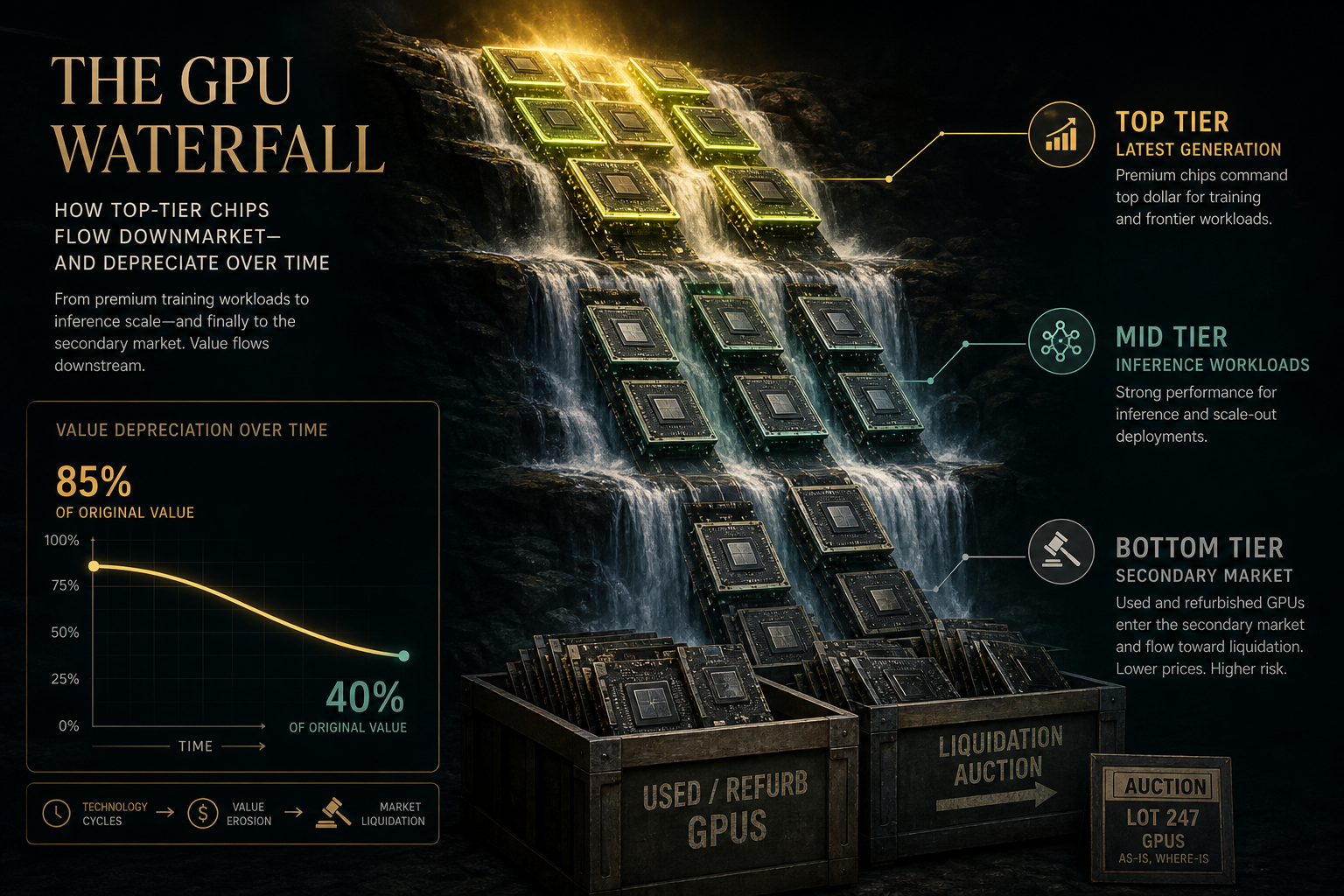

Silicon ages faster than concrete. The secondary market for H100 GPUs has matured into a real pricing signal: units 18 to 30 months old trade at 75 to 85 percent of list; by 36 months the range widens to 40 to 75 percent depending on Blackwell supply. Refurbished cards clear at $18,000 to $22,000 with limited warranty. Rental rates on H100s have compressed from roughly $8 per GPU-hour toward $2 as supply expanded.

Operators use depreciation schedules of four to six years. NVIDIA’s chip cycle implies two to three years of frontier relevance. Michael Burry’s estimate of $176 billion in understated industry depreciation between 2026 and 2028 is controversial but directionally instructive: accounting life and economic life diverge.

When utility disappoints, equipment follows a cascade:

- Frontier training clusters absorb the newest accelerators first.

- Inference and fine-tuning absorb the previous generation at lower hourly rates.

- Research, batch, and emerging-market neoclouds buy secondary hardware at discounts.

- Distressed sellers liquidate at $14,000 to $18,000 per card; lenders with GPU-backed collateral enforce dynamic loan-to-value covenants.

CoreWeave reported H100s from 2022 contract expirations rebooking at 95 percent of original pricing in late 2025 — evidence the cascade can work while enterprise demand exceeds supply. If demand stalls, the cascade becomes a cliff: chips do not rust, but their revenue per watt falls below the power bill.

Repurposing is partial, not magical. GPUs can serve inference after training moves on. Rows designed for 100-kilowatt racks cannot become generic colocation without capital surgery. Aging gear also draws more power per flop — a hidden stranded cost even when racks stay lit.

The Verdict the Math Allows

AI applications do have enough utility to justify some of the current spend — concentrated in enterprise workflows, developer APIs, and supplier tiers with take-or-pay contracts. They do not yet have enough consumer utility, measured by conversion and retention, to justify building as if every weekly active user were a future subscriber.

If consumer utility fails to catch up, the outcome is not a single dramatic collapse. It is a selective reckoning: ghost warehouses where power and architecture misalign; GPU fleets marked down through secondary markets while accountants argue over useful life; hyperscalers pivoting from land-grab capex to utilization discipline; and survivors owning sites with fiber, power, and flexible thermal design rather than single-generation GPU cathedrals.

The dot-com lesson was not that the internet was fake. It was that financing assumed monetization on a faster clock than behavior changed. AI’s clock is running on inference hours billed, not parameter counts trained.

For readers tracking the sector, the actionable frame is simple: watch paying-user growth against megawatt growth, not demo virality against model releases. When the first number lags the second, the warehouses do not stay empty — they stay expensive. And the equipment inside them ages on schedule, whether or not anyone renewed this month.

Tags

Sources

Analysis based on OpenAI and ChatGPT user and revenue disclosures (2025–2026), enterprise versus consumer retention data, Microsoft data center deferrals, Deloitte inference workload estimates, GPU secondary market pricing (Hashrate Index, Mercatus, Compute Forecast), enterprise GPU utilization surveys, and BIS circular-finance warnings on AI capex